HRCCU is part of the UsNet Shared Branch Network This provides you, our member, greater convenience and real-time access to your accounts when traveling around the corner or across the country.

Finance, just like the economy, is an ever-changing landscape, making it hard for many to navigate.

But there are some age-old rules about money that are always dependable, right?

Not necessarily.

Many financial planning guidelines once considered unfailing have since become financial myths, irrelevant to today.

Basing decisions on these outdated or inaccurate personal finance myths is not only unreliable but potentially harmful to a person’s overall financial wellbeing.

In fact, there are many personal finance myths that result in long-term consequences and can stagger an individual’s financial growth — especially when it comes to borrowing and saving.

Therefore, it’s crucial to remain aware of common financial planning myths that may be affecting your personal financial health.

Allow us to debunk the top five common financial myths to help you make better personal finance choices.

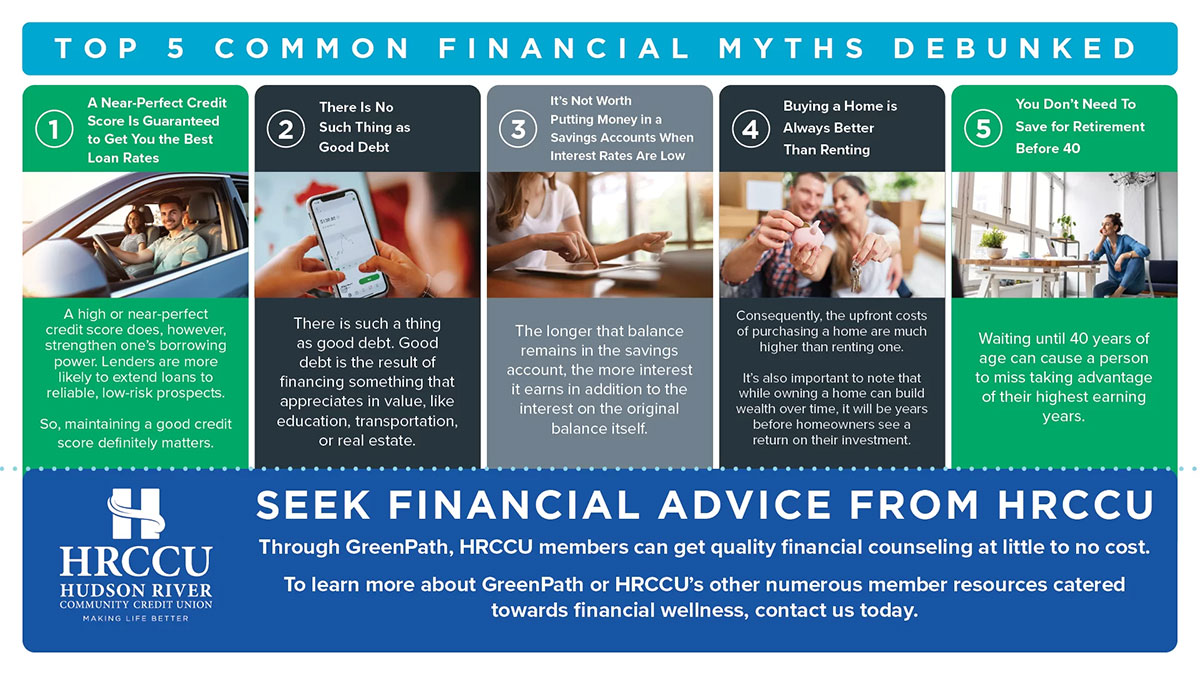

1. A Near-Perfect Credit Score Is Guaranteed to Get You the Best Loan Rates

Although this financial myth holds some weight, it’s not completely accurate because loan approval and rates vary depending on the lender, the type of loan, loan terms, and other elements.

Yes, a credit score is one of multiple determining factors of loan amounts. But it’s not always the most important — nor is it guaranteed to make lenders approve a loan or grant the best loan rate.

A high or near-perfect credit score does, however, strengthen one’s borrowing power. Lenders are more likely to extend loans to reliable, low-risk prospects.

So, maintaining a good credit score definitely matters.

However, it’s not a confirmation of approval. There are numerous reasons lenders disapprove applicants with near-perfect credit scores.

Such factors include the prospect’s annual income, current amount of debt, or employment history.

Ultimately, a good credit score represents financial responsibility but not a supreme monetary status that assures 100% loan approval at the best rates.

2. There Is No Such Thing as Good Debt

In other words, all debt is bad — or so one thinks.

In actuality, there is such a thing as good debt. Good debt is the result of financing something that appreciates in value, like education, transportation, or real estate.

Debt in manageable amounts can be empowering to one’s financial responsibility, planning, and credit score. This is of course, as long as the debt is regularly paid down or off on time each pay period.

Accumulating some debt can also be the key to financial freedom. By borrowing to finance a small business or student loan, individuals are setting themselves up for higher earnings in the future.

Additionally, interest on certain types of loans, such as a mortgage, is lower and tax-deductible, unlike interest on personal loans.

Plus, those with good credit as a result of paying off debt become eligible for credit cards with strong rewards programs.

A rewards credit card involves a point system. Every time the card is used, points are earned.

These points can then be exchanged for benefits such as airfare or travel miles, access to high-cost events like concerts, and even money back on everyday purchases like groceries or gas.

3. It’s Not Worth Putting Money in a Savings Accounts When Interest Rates Are Low

This major personal finance myth is easy to believe because of how low savings rates have fallen, leading many to wonder if a savings account and its maintenance fees is worth it.

Don’t forget, however, to look at the compound interest.

Compound interest is interest earned on money saved which in turn also receives interest over time. For instance, a balance of $1,000 in a savings account may earn 0.05% in annual interest.

But the longer that balance remains in the savings account, the more interest it earns in addition to the interest on the original balance itself.

Alternatively, there are other types of savings accounts that offer more competitive savings rates, such as certificates of deposits (CDs).

CDs guarantee a specific interest rate for a certain length of time. No matter how the national savings rate may fluctuate, a CD will continue to earn the same interest rate throughout its term.

The CDs offered by HRCCU can reach terms of up to 60 months with just a $500 deposit. These long-term CDs earn an interest rate of 0.45% with minimal maintenance fees.

4. Buying a Home is Always Better Than Renting

A financial myth that, as with most of the ones on this list, is only partially true.

Indeed, buying a home is generally a great, long-term investment, but only if the purchaser is ready to finance it, settle down, and commit.

There are a lot of factors that go into purchasing a home, aside from the mortgage. Buyers must also consider property taxes, possible homeowner association (HOA) fees, and maintenance costs.

Consequently, the upfront costs of purchasing a home are much higher than renting one.

It’s also important to note that while owning a home can build wealth over time, it will be years before homeowners see a return on their investment.

And for individuals with outstanding debt, affording a home may not even be a viable option.

Debt vastly affects debt-to-income (DTI) ratio. DTI ratio is calculated by dividing the sum of a borrower’s monthly debt payments into the gross monthly income. This information is used to help determine a borrower’s eligibility and monthly mortgage payment.

Renting from a financial standpoint is typically a more accessible option, at least in the short-term. This is because the fees are less complex.

Those who rent are able to put money towards other financial needs or investments such as paying down debt, saving, building emergency funds, and growing investment portfolios.

The idea of buying being the better option over renting a home is a financial planning myth because it’s not a one-size-fits-all solution.

5. You Don’t Need To Save for Retirement Before 40

On the contrary, it’s never too early to start saving for retirement.

Waiting until 40 years of age can cause a person to miss taking advantage of their highest earning years.

Putting away money for retirement early allows those savings more time to compound interest or grow in value.

But waiting until the age of 40 to save for retirement means less time to accumulate compound interest.

Through GreenPath, HRCCU members can get quality financial counseling at little to no cost.

Services, such as debt counseling and standard student loan counseling are completely free for GreenPath clients.

Other affordable resources available at GreenPath include homebuyer counseling, reverse mortgage counseling, and comprehensive online classes on money management.

GreenPath consultants provide clients with knowledge and advice that not only suits their current financial situation, but also improves it.

To learn more about GreenPath or HRCCU’s other numerous member resources catered towards financial wellness, contact us today.